Finances

Rising Up to Meet Pandemic’s Financial Challenges

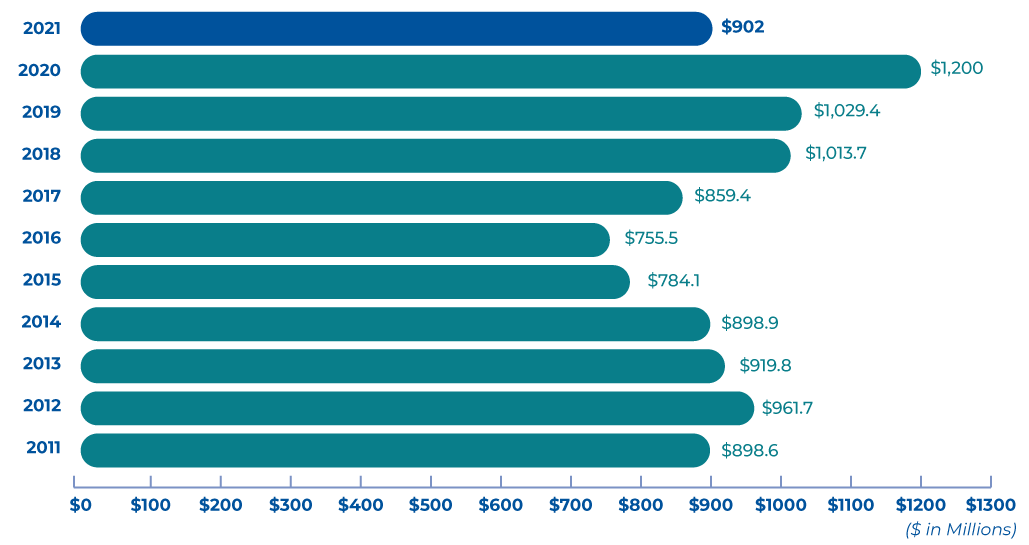

The pandemic’s far-reaching influence presented a host of financial challenges for Memorial Healthcare System in fiscal 2021.

“Our finances followed the waves of COVID,” said David Smith, Executive Vice President and Chief Financial Officer, who explained that operating margins dipped with each surge and improved as waves receded.

“We remain financially strong,” Mr. Smith stressed. “But overall, results were less than we expected from operations for the year.”

A large factor in that was the significant increase in operating costs. In a surge month, he said, total expenses increased by 15% to 20% over the previous year.

Consider PPE. Memorial caregivers and cleaning staff needed a large amount of N95 masks, gowns, gloves and face shields — all of these items had to be changed between every patient. The sheer amount of PPE is expensive, and when supply chain issues made items scarce, the costs got even higher.

For example, Smith said, when the world’s largest medical glove manufacturer in Malaysia shut down its largest factory because of COVID-19, the cost of gloves nearly quadrupled. And Memorial uses “hundreds of thousands of gloves on a daily basis,” he said.

Staffing costs increased as well. Memorial offered caregivers well-deserved hazard pay and incentives for extra shifts. As stress and burnout built, however, employees needed a break. Some even left healthcare altogether. For the first time in years, Memorial supplemented its workforce with agency labor — and agency rates increased by 300%.

Where many Florida businesses were forced to furlough employees, Memorial took steps to prevent this drastic measure. Mandatory flex days were instituted at the height of the surge, matching contributions to employee retirement accounts were temporarily suspended, a hiring freeze was temporarily mandated to protect existing employees and leadership merit increases were temporarily deferred.

Of course, discretionary spending was paused and significantly tightened up as well.

As a financially sound healthcare system, “we try to make sound decisions. We do the things we need to do to maintain financial stability,” Smith said. He credits strong leadership and support from the board to spend the funds necessary to provide quality healthcare for patients and to protect employees.

“We’re here for our patients, our community and our employees,” Smith said. “We will continue to look for ways to do the right thing for all of them.”

Strong Bond Rating

Despite the challenging year, Memorial Healthcare System remains one of only three health systems in Florida with an AA bond rating. Factors such as strong cash flow and a strong balance sheet influence this rating.

VIP 2.0

The Value Improvement Program, which hit its first cost-savings goal ahead of schedule in 2020, has reached about $40 million of a new $100 million goal. Progress continues at a slower pace as COVID-19 remains the priority.

COVID-19 EXPENSES: ~ $20 million on COVID-19-specific supplies alone

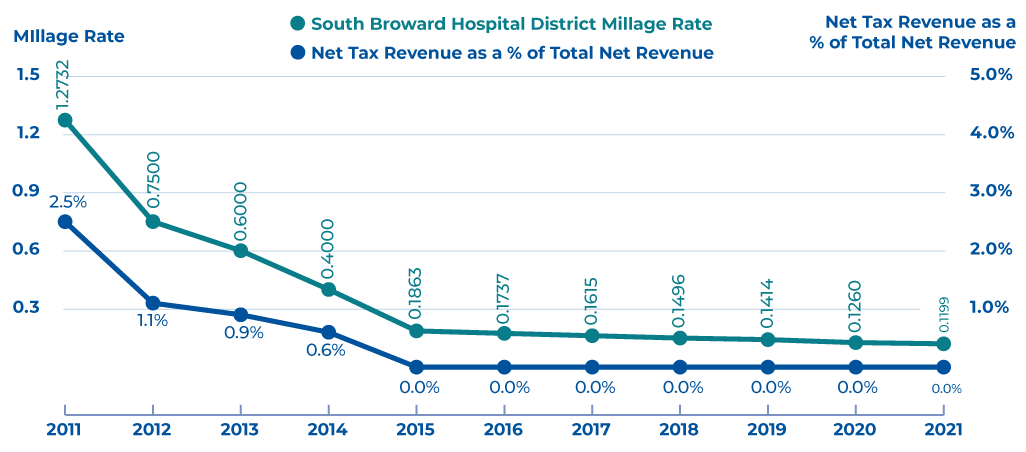

MILLAGE RATE

UNCOMPENSATED CARE

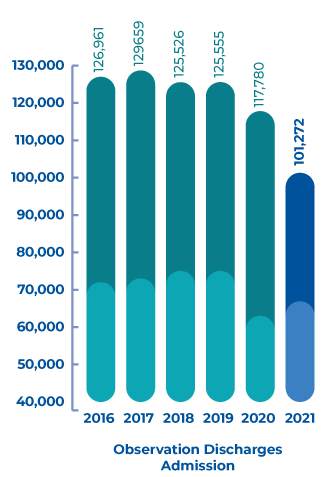

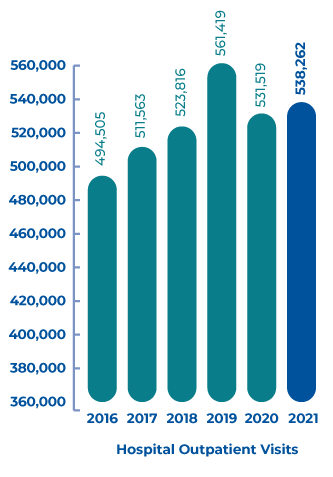

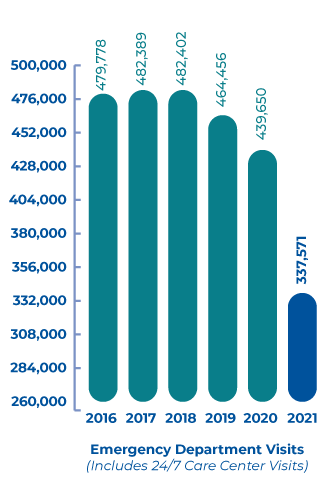

PATIENT VOLUME